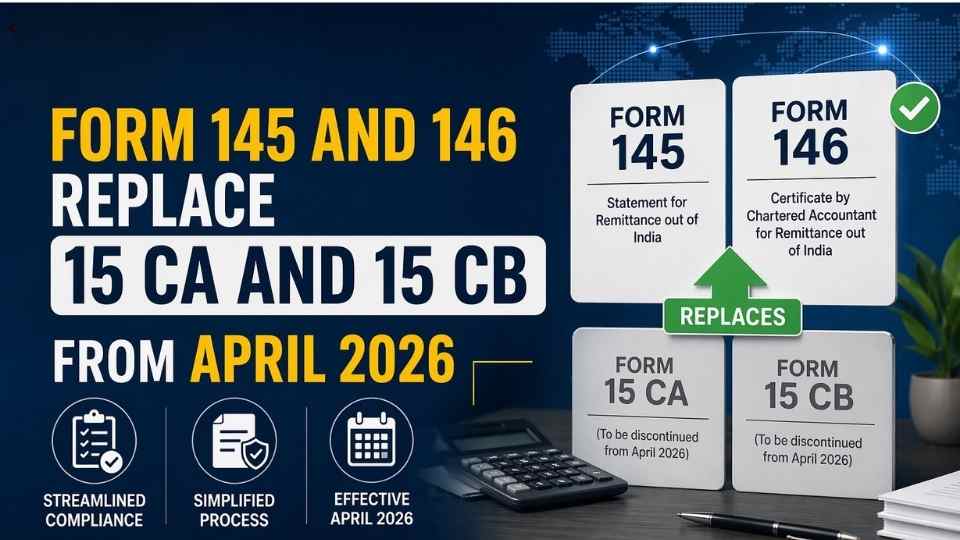

The Income Tax Department is changing the way people report foreign money transfers starting in April 2026. They are using forms called Form 145 and Form 146 instead of the old Form 15CA and Form 15CB.

This change shows that the government wants to make tax reporting easier to do on computers get rid of work and make sure foreign money transfers are honest and clear.

Existing Framework: Form 15CA & 15CB

Under the system:

• Form 15CA was a self-declaration that the person making the payment had to file

• Form 15CB was a certificate that a Chartered Accountant had to issue

These forms made sure that the person making the payment followed Section 195 of the Income-tax Act, 1961 which is about Tax Deducted at Source (TDS), on payments made to people who do not live in India.

Need for Reform in Foreign Remittance Compliance

Over time, several challenges emerged:

- Duplication of information between forms

- Manual intervention and dependency on professionals

- Lack of real-time validation

- Increased compliance burden for businesses

- Limited integration with banking and tax systems

To address these issues, a more robust, technology-driven framework was introduced.

Introduction of Form 145 & Form 146

Form 145 – Statement of Foreign Remittance

- To be filed by the remitter

- Captures complete details of the transaction

- Integrated with income tax systems for validation

Form 146 – Chartered Accountant Certificate

- Issued by a practicing CA

- Certifies taxability, TDS applicability, and DTAA benefits

- Replaces Form 15CB with enhanced reporting standards

Key Features of the New Forms

- Fully online and system-driven filing

- Pre-filled data from income tax records

- Automated error checks and validation

- Improved tracking of foreign remittances

- Better alignment with global tax compliance standards

Comparative Analysis: Old vs New System

| Basis | Form 15CA/15CB | Form 145/146 |

| Nature | Partially manual | Fully digital |

| Data Entry | Repetitive | Streamlined & pre-filled |

| Validation | Limited | Automated system checks |

| Integration | Standalone | Integrated with IT portal |

| Compliance Burden | Higher | Reduced |

| Transparency | Moderate | High |

Applicability & Scope

Form 145 & 146 are applicable in cases of:

- Payments made to non-residents

- Remittances outside India

- Transactions chargeable to tax under Indian law

Not Applicable When:

- Remittance is not taxable

- Covered under specified exemption categories

- Listed in RBI’s exempt remittance list

Situations Where Form 145 is Required

Form 145 is required:

- Before initiating foreign remittance

- For both taxable and certain non-taxable payments

- In all cases where reporting is mandated under tax rules

Requirement of Form 146 (CA Certificate)

Form 146 becomes mandatory in:

- Cases involving taxability determination

- Where DTAA benefits are claimed

- Complex or high-value transactions

- Situations requiring professional certification

Step-by-Step Filing Procedure

- Login to Income Tax e-Filing Portal

- Navigate to e-File → Foreign Remittance Compliance

- Select Form 145

- Enter remittance details (payer, payee, nature, amount)

- Upload Form 146 (if applicable)

- Validate details through system checks

- Submit using DSC/EVC

- Generate acknowledgment for records

Documentation & Reporting Requirements

- PAN of remitter

- Details of non-resident payee

- Nature and purpose of remittance

- Invoice / Agreement copy

- Tax Residency Certificate (TRC)

- DTAA working (if applicable)

- TDS calculation sheet

12. Key Compliance Considerations

- Correct classification of remittance nature is critical

- Ensure accurate TDS deduction under Section 195

- Maintain proper documentation for scrutiny

- Reconcile remittance details with books of accounts

- Keep CA certification aligned with actual transaction

13. Impact on Businesses & Professionals

For Businesses

- Reduced compliance complexity

- Faster processing of remittances

- Lower chances of rejection

For Chartered Accountants

- Increased accountability

- More detailed certification responsibility

- Greater reliance on professional judgment

14. Penalty & Consequences of Non-Compliance

Non-compliance may lead to:

- Penalty under the Income-tax Act

- Disallowance of expenditure under Section 40(a)(i)

- Delay or rejection of remittance by banks

- Departmental notices and scrutiny

Practical Illustrations

Case 1: Payment for Technical Services (USA)

- Taxable under Indian law

- Requires TDS deduction

- Form 145 + Form 146 mandatory

Case 2: Import of Goods

- Generally, not taxable

- Form 145 required (subject to reporting rules)

- Form 146 may not be required

Case 3: Royalty Payment with DTAA Benefit

- Lower tax rate claimed

- Form 146 mandatory for certification

Conclusion

The introduction of Form 145 and Form 146 is a change for foreign remittances in India. This change means that foreign remittances in India will now be handled in a transparent and efficient way.

Foreign remittances in India will really benefit from this system. Businesses need to get ready for this system of foreign remittances in India by doing a few things. They need to:

- Make sure they have all the documents for foreign remittances in India

- Get the tax right for foreign remittances in India

• Work closely with professionals who know about foreign remittances, in India

FAQs

Q1. From when are Form 145 & 146 applicable?

From April 2026 onwards.

Q2. Are Form 15CA and 15CB still valid?

No, they have been replaced by Form 145 and Form 146.

Q3. Is Form 146 required in every case?

No, only where certification is required.

Q4. Who files Form 145?

The remitter (payer making foreign payment).

Q5. Can remittance be made without filing Form 145?

No, banks may not process such transactions.

Q6. What is the role of a Chartered Accountant?

To certify taxability, TDS applicability, and DTAA claims via Form 146.

Q7. Is there any penalty for wrong filing?

Yes, penalties and disallowances may apply.

Q8. Are exempt transactions also required to be reported?

Certain exempt transactions may still require reporting under Form 145.

ALSO READ

MCA Streamlines Email ID Update Process for Companies and LLPs on MCA21 Portal

The ‘User Affidavit’ in Trademarks: Why ‘Proposed to be Used’ Is a Risky Bet

Drafting a Founders’ Agreement: 5 Clauses That Prevent “Founder Fallout”

Crowdfunding Rules for NGOS in India