Annual filing under the Companies Act, 2013 is a mandatory requirement for all companies registered in India. Among the many compliance forms, two of the most significant are AOC-4 and MGT-7.

At first glance, both may look similar because they are part of the annual filing cycle, but they serve distinct purposes. AOC-4 focuses on financial reporting, while MGT-7 captures corporate governance details.

In this blog, we will understand the difference between AOC-4 and MGT-7, their due dates, penalties, and why they are important.

1. Legal Provisions

- AOC-4 – Governed by Section 137 of the Companies Act, 2013 and Rule 12 of the Companies (Accounts) Rules, 2014.

- MGT-7 – Governed by Section 92 of the Companies Act, 2013 and Rule 11 of the Companies (Management and Administration) Rules, 2014.

2. Purpose of Filing

- AOC-4: To submit audited financial statements and related reports of the company. It highlights the financial performance and position of the company during a financial year.

- MGT-7: To submit the annual return, which includes details of the company’s shareholding, directors, and corporate governance matters.

3. Applicability

- AOC-4: Applicable to all companies including Private Limited, Public Limited, One Person Company (OPC), and Section 8 Companies.

- MGT-7: Applicable to all companies, but for Small Companies and OPCs, a simplified version called MGT-7A is used.

4. Due Dates

- AOC-4: Must be filed within 30 days from the conclusion of the AGM.

- If AGM not held – within 30 days from the date the AGM should have been held.

- For OPCs – within 180 days from the end of the financial year.

- MGT-7: Must be filed within 60 days from the conclusion of the AGM.

- If AGM not held – within 60 days from the date the AGM should have been held.

5. Filing Authority & Certification

- AOC-4:

Filed by the Director of the company.

Certification required:

- For small companies and OPCs – Digital signature of a director is sufficient.

- For other companies (non-small companies) -It must be certified by a Practicing Professional (CA/CS/CMA).

MGT-7:

Requires the digital signature of a director/company secretary.

Certification required:

- For listed companies and other non-small companies – Mandatory certification by a Practicing Company Secretary (PCS).

- For small companies and OPCs – Certification is not required.

6. Key Information Contained

- AOC-4 (Financial Details):

- Balance Sheet as at the end of the financial year

- Profit & Loss Account

- Cash Flow Statement (if applicable)

- Notes to Financial Statements

- Statement of Change in Equity

- Auditor’s Report & Directors’ Report

- CSR (Corporate Social Responsibility) details (if applicable)

MGT-7 (Non-Financial/Corporate Details):

- Registered office, principal business activities, and holding/subsidiary/associate companies

- Shareholding pattern (promoters, public, institutional, etc.)

- Details of shares, debentures, and other securities issued during the year

- Indebtedness of the company

- List of directors and key managerial personnel (KMP)

- Details of meetings held (Board/AGM/EGM)

- Certification by Company Secretary (if required)

7. Penalty for Non-Compliance of AOC-4 (Filing of Financial Statements) – Section 137

₹100 per day for each day the default continues.

8. Penalty for Non-Compliance of MGT-7 / MGT-7A (Filing of Annual Return) -Section 92

Further ₹100 per day for each day the default continues.

The Companies (Accounts) Second Amendment Rules, 2025, effective from 14 July 2025, streamlined filing requirements for AOC-4 and related forms but did not alter the penalty amounts. Thus, timely filing remains critical to avoid heavy fines.

8. Filing Process

AOC-4:

- Prepare financial statements and have them audited.

- Conduct the AGM and get approval of financials.

- File AOC-4 electronically on MCA portal with digital signatures and attachments (Auditor’s Report, Balance Sheet, etc.).

MGT-7:

- Compile data related to shareholding, directors, and meetings.

- Ensure accuracy with records maintained in registers.

- File MGT-7 electronically on MCA portal within due date.

9. Practical Example

- Suppose a company named XYZ Pvt Ltd holds its AGM on 30th September 2025:

- AOC-4 – Must be filed on or before 29th October 2025.

- MGT-7 – Must be filed on or before 29th November 2025.

- This shows that AOC-4 is always filed before MGT-7 in the compliance cycle.

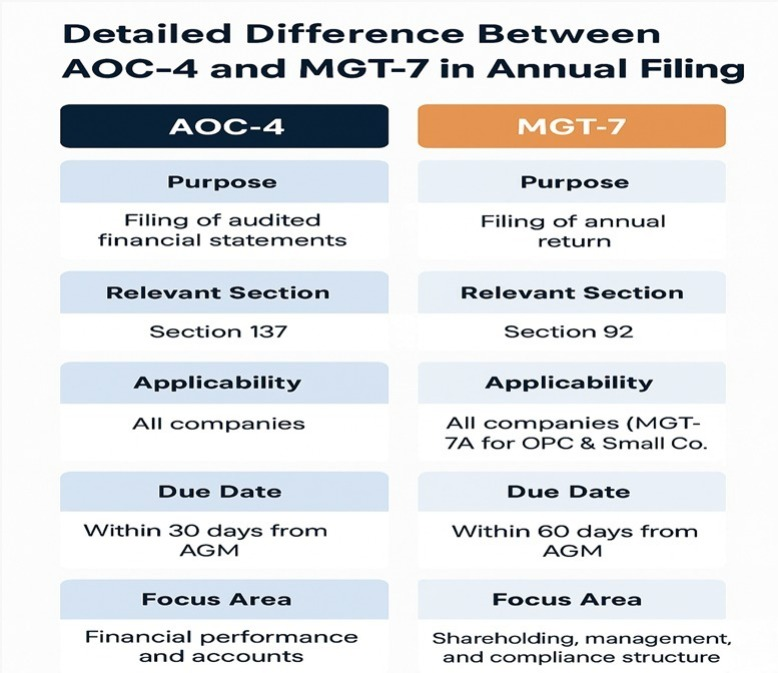

Key Difference Between AOC-4 and MGT-7

| Particulars | AOC-4 | MGT-7 |

| Purpose | Filing of audited financial statements | Filing of annual return |

| Relevant Section | Section 137 | Section 92 |

| Applicability | All companies registered under Companies Act | All companies (except OPC & Small Companies which file MGT-7A) |

| Due Date | Within 30 days from AGM | Within 60 days from AGM |

| Focus Area | Financial performance & accounts | Shareholding, management, and compliance structure |

| Certification | By Director/Practicing Professional (in certain cases) | Certification by Company Secretary in practice (mandatory for listed/large companies/non small cos) |

Importance of Timely Filing AOC-4 and MGT-7

Timely filing of both these forms ensures that the company remains legally compliant and avoids heavy penalties. Non-filing may also lead to the disqualification of directors and even prosecution in extreme cases.

- AOC-4 helps stakeholders analyze the financial health of the company.

- MGT-7 provides transparency about the ownership and management structure.

Conclusion

Both AOC-4 and MGT-7 are equally important forms in the annual compliance calendar of a company. While AOC-4 deals with financial transparency, MGT-7 ensures governance transparency.

Filing these forms within due dates not only prevents heavy penalties but also reflects a company’s commitment towards good corporate governance and regulatory compliance.

Frequently Asked Questions (FAQs)

1. What is the difference between AOC-4 and MGT-7?

AOC-4 is used to file the audited financial statements of a company, while MGT-7 is used to file the annual return, which includes shareholding, directors, and company structure details.

2. Who is required to file AOC-4?

All companies registered under the Companies Act, 2013, including Private Limited, Public Limited, One Person Company (OPC), and Section 8 Companies, are required to file AOC-4.

3. Who is required to file MGT-7?

Every company needs to file MGT-7. However, Small Companies and OPCs file a simplified version called MGT-7A.

4. What is the due date for filing AOC-4 and MGT-7?

- AOC-4 – Within 30 days from the date of AGM.

- MGT-7 – Within 60 days from the date of AGM.

ALSO READ

Difference Between MOA and AOA Explained Simply

How to Increase Authorized Share Capital of a Company

Step-by-Step Guide for Closing a Nidhi Company